SMM July 1st News:

Metal Market:

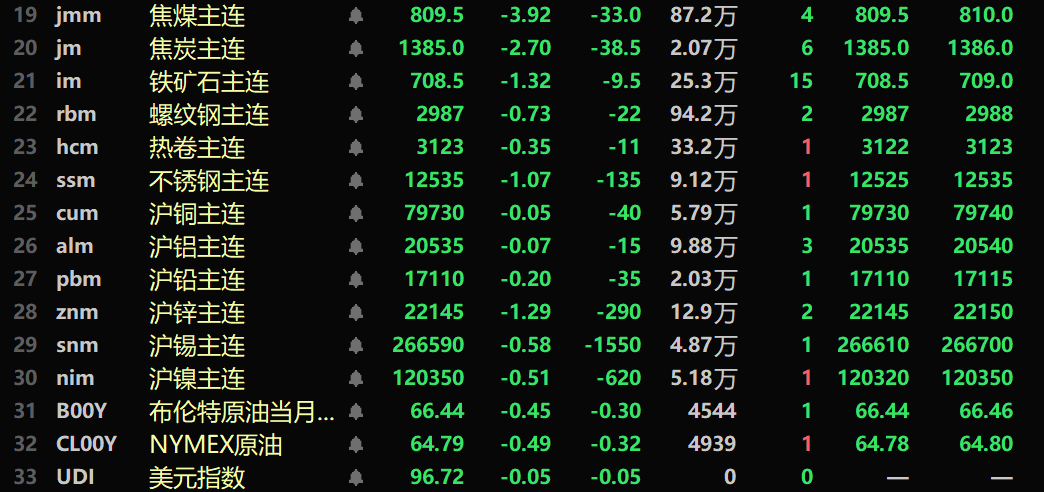

As of the midday close, domestic base metals fell across the board, with SHFE copper down 0.05%, SHFE nickel down 0.51%, SHFE aluminum down 0.07%, SHFE zinc down 1.29%, SHFE tin down 0.58%, and SHFE lead down 0.2%.

Additionally, the most-traded aluminum futures fell slightly, while the most-traded alumina futures dropped 2.01%. Lithium carbonate fell 1.95%, silicon metal fell 4.31%, and polysilicon fell 2.78%.

The ferrous metals series all rose, with iron ore down 1.32%, rebar down 0.73%, HRC down 0.35%, and stainless steel down 1.07%. Coking coal and coke: coking coal fell 3.92%, coke fell 2.7%.

Overseas metals: As of 11:39 a.m., LME metals generally declined, though LME copper and LME aluminum edged up by less than 0.1% each. LME nickel fell 0.26%, LME zinc fell 0.94%, LME tin fell 0.24%, and LME lead fell 0.17%.

Precious metals: As of 11:39 a.m., COMEX gold rose 0.74%, COMEX silver rose 0.02%; domestically, SHFE gold rose 1.04%, and SHFE silver rose 0.09%.

As of the midday close, the most-traded Europe container shipping futures contract rose 0.74% to 1,780.1 points.

Partial futures midday quotes as of July 1st 11:39 a.m.:

》July 1st SMM Metal Spot Prices

Spot and Fundamentals

Zinc: Ningbo market mainstream brand 0# zinc transaction prices ranged between 22,280-22,470 yuan/mt. Ningbo conventional brands quoted a premium of 55 yuan/mt against the 2507 contract and a 20 yuan/mt premium against Shanghai spot prices, with mainstream Ningbo region quotes referencing the 2507 contract... 》Click for details

Macro Front

Domestic:

[China's Caixin manufacturing PMI rose to 50.4 in June, returning to expansion territory] The June Caixin China manufacturing purchasing managers' index (PMI) was released today at 50.4, up 2.1 percentage points from May and matching April's level, returning above the threshold. (Finance News)

The People's Bank of China conducted 131 billion yuan in 7-day reverse repo operations at an interest rate of 1.4%, unchanged from previous operations. With 406.5 billion yuan in 7-day reverse repos maturing today, the net withdrawal reached 275.5 billion yuan.

US Dollar:

As of 11:39 a.m., the US dollar index fell 0.05% to 96.72. As US President Trump once again called for an interest rate cut, the market awaited employment market data later this week to assess the potential trajectory of interest rate cuts by the US Fed. On June 30 local time, US President Trump posted on social media, stating that "Mr. Too Late" Fed Chairman Powell and the entire committee should be ashamed for not cutting interest rates. Trump said that if they had done their job properly, "the US could have saved trillions of yuan in interest costs," "but the committee just stood by, so they are also to blame." Trump stated that the US should pay an interest rate of 1%. US Treasury Secretary Bentsen said on Monday that the Trump administration was considering using the next Fed governor vacancy, expected to occur in early 2026, to appoint a successor to Chairman Powell.

Atlanta Fed President Bostic reiterated on Monday that he still expects the Fed to cut interest rates once this year, while stating that there is no urgency to take action as there remains much uncertainty about how tariffs will affect the inflation dynamics of the US economy. Meanwhile, Chicago Fed President Goolsbee believes that stagflation will not occur, but there is certainly a possibility of simultaneous deterioration in inflation and employment.

Meanwhile, US President Trump expressed disappointment on Monday over US-Japan trade negotiations. Meanwhile, US Treasury Secretary Bentsen warned that despite sincere negotiations, countries may receive notifications of significantly higher tariffs as the July 9 deadline approaches. (Webstock Inc.)

Data:

Today, data including China's June Caixin Manufacturing PMI, France's final June SPGI Manufacturing PMI, Germany's final June SPGI Manufacturing PMI, the Eurozone's final June SPGI Manufacturing PMI, the UK's final June SPGI Manufacturing PMI, the Eurozone's preliminary June Harmonized CPI Year-on-Year Rate - Unadjusted, the Eurozone's preliminary June Core Harmonized CPI Year-on-Year Rate - Unadjusted, the US's final June SPGI Manufacturing PMI, the US's June ISM Manufacturing PMI, the US's May JOLTs Job Openings, and Mexico's June SPGI Manufacturing PMI will be released.

In addition, it is worth noting that on July 1: The Hong Kong Stock Exchange will be closed for one day on July 1 due to the Hong Kong Special Administrative Region Establishment Day holiday, with northbound and southbound trading suspended. Also to be watched: Speeches by 2025 FOMC voting member and Chicago Fed President Goolsbee; a speech by ECB President Lagarde; a panel discussion by global central bank governors (Fed Chairman Powell, ECB President Lagarde, Bank of England Governor Bailey, Bank of Japan Governor Ueda Kazuo, and Bank of Korea Governor Lee Chang-yong); and the ECB's Central Banking Forum held in Sintra.

Crude Oil:

Both oil futures dropped slightly, with US crude oil down 0.49% and Brent crude oil down 0.45% as of 11:39 AM. Oil prices remained under pressure amid concerns over OPEC's expected production increase in August and potential economic slowdown due to US tariff hike prospects.

Data from the US Energy Information Administration's (EIA) *Petroleum Supply Monthly* showed US crude oil production reached a record high of 13.47 million bpd in April, surpassing March's 13.45 million bpd. The EIA had previously estimated March production at 13.49 million bpd.

Preliminary surveys released Monday indicated expected declines in US crude oil and distillate inventories last week, alongside anticipated gains in gasoline stockpiles. The average forecast from four surveyed analysts showed US crude oil inventories likely fell by approximately 230,000 barrels in the week ending June 27. The American Petroleum Institute (API) will release its weekly inventory report at 4:30 AM Beijing time on Wednesday, while the EIA will publish its data at 10:30 PM Beijing time on the same day. (Webstock Inc.)

Spot Market Overview:

►Ningbo Zinc: Kirin zinc ingot arrivals keep premium stable [SMM Midday Review]

Other metal spot market reviews to be updated later, please refresh to view